The Affordable Care Act (ACA) has made a number of significant changes to group health plans since the law was enacted in 2010. Since that time, a number of changes have been made to various ACA requirements that employers and plan sponsors should be aware of. It is important for employers to periodically review their benefit plans in order to maintain compliance with these various requirements.

The Affordable Care Act (ACA) has made a number of significant changes to group health plans since the law was enacted in 2010. Since that time, a number of changes have been made to various ACA requirements that employers and plan sponsors should be aware of. It is important for employers to periodically review their benefit plans in order to maintain compliance with these various requirements.

Changes to some ACA requirements take effect in 2021 for employers sponsoring group health plans, such as increased dollar limits. To prepare for 2021, employers should review these upcoming requirements and develop a compliance strategy.

This ACA Overview provides an ACA compliance checklist for 2021. Please contact Reseco Group for assistance or if you have questions about changes that were required in previous years.

Links and Resources

• U.S. Department of Health and Human Services’ (HHS) Final Notice of Benefit & Payment Parameters for 2021 established the cost-sharing limits for 2021.

• Internal Revenue Service (IRS) Revenue Procedure 2020-36 indexed the affordability contribution percentages for 2021.

Plan Design Changes

The following plan design requirements have changed for 2021:

- Limits on cost-sharing for essential health benefits

- Coverage affordability percentages under the employer shared responsibility rules

Health flexible spending account (FSA) salary contribution limits are also expected to change for 2021.

Penalty Calculations

The following amounts related to ACA penalties have changed for 2021:

- Maximum penalties for ACA reporting violations

- Dollar amounts for calculating employer shared responsibility penalties

Plan Design Changes

Grandfathered Plan Status

A grandfathered plan is one that was already in existence when the ACA was enacted on March 23, 2010. If you make certain changes to your plan that go beyond permitted guidelines, your plan is no longer grandfathered. However, grandfathered status does not automatically expire as of a specific date. A plan may maintain its grandfathered status as long as no prohibited changes are made. Once a plan relinquishes grandfathered status, it cannot be regained and the plan must comply with additional reforms under the ACA.

Contact Reseco Group if you have questions about changes you have made, or are considering making, to your plan.

Review your plan’s grandfathered status:

- If you have a grandfathered plan, determine whether it will maintain its grandfathered status for the 2021 plan year. Grandfathered plans are exempt from some of the ACA’s mandates. A grandfathered plan’s status will affect its compliance obligations from year to year.

- If your plan will lose its grandfathered status for 2021, confirm that the plan has all of the additional patient rights and benefits required by the ACA for non-grandfathered plans. This includes, for example, coverage of preventive care without cost-sharing requirements.

- If your plan will keep its grandfathered status, continue to provide the Notice of Grandfathered Status in any plan materials provided to participants and beneficiaries that describe the benefits provided under the plan (such as the plan’s summary plan description and open enrollment materials). Model language is available.

Cost-Sharing Limits

Effective for plan years beginning on or after Jan. 1, 2014, non-grandfathered health plans are subject to limits on cost sharing for essential health benefits (EHB). The ACA’s overall annual limit on cost sharing (also known as an out-of-pocket maximum) applies for all non-grandfathered group health plans, whether insured or self-insured. Under the ACA, a health plan’s out-of-pocket maximum for EHB may not exceed $8,550 for self-only coverage and $17,100 for family coverage, effective for plan years beginning on or after Jan. 1, 2021.

Health plans with more than one service provider may divide the out-of-pocket maximum across multiple categories of benefits, rather than reconciling claims across multiple service providers. Thus, health plans and issuers may structure a benefit design using separate out-of-pocket maximums for EHB, provided that the combined amount does not exceed the annual out-of-pocket maximum limit for that year. For example, in 2021, a health plan’s self-only coverage may have an out-of-pocket maximum of $6,000 for major medical coverage and $2,550 for pharmaceutical coverage, for a combined out-of-pocket maximum of $8,550.

Beginning with the 2016 plan year, the self-only annual limit on cost sharing applies to each individual, regardless of whether the individual is enrolled in self-only coverage or family coverage. This embeds an individual out-of-pocket maximum in family coverage so that an individual’s cost sharing for essential health benefits cannot exceed the ACA’s out-of-pocket maximum for self-only coverage.

Note that the ACA’s cost-sharing limit is higher than the out-of-pocket maximum for high deductible health plans (HDHPs). In order for a health plan to qualify as an HDHP, the plan must comply with the lower out-of-pocket maximum limit for HDHPs. HHS provided FAQ guidance on how this ACA rule affects HDHPs with family deductibles that are higher than the ACA’s cost-sharing limit for self-only coverage.

According to HHS, an HDHP that has a $10,000 family deductible must apply the annual limitation on cost sharing for self- only coverage ($8,550 in 2021) to each individual in the plan, even if this amount is below the $10,000 family deductible limit. Because the $8,550 self-only maximum limitation on cost sharing exceeds the 2021 minimum annual deductible amount for HDHPs ($2,800), it will not cause a plan to fail to satisfy the requirements for a family HDHP.

Check your plan’s cost-sharing limits:

- Review your plan’s out-of-pocket maximum to make sure it complies with the ACA’s limits for the 2021 plan year ($8,550 for self-only coverage and $17,100 for family coverage).

- If you have an HSA-compatible HDHP, keep in mind that your plan’s out-of-pocket maximum must be lower than the ACA’s limit. For 2021, the out-of-pocket maximum limit for HDHPs is $7,000 for self-only coverage and $14,000 for family coverage.

- If your plan uses multiple service providers to administer benefits, confirm that the plan will coordinate all claims for EHBs across the plan’s service providers, or will divide the out-of-pocket maximum across the categories of benefits, with a combined limit that does not exceed the maximum for 2021.

- Confirm that the plan applies the self-only maximum to each individual in the plan, regardless of whether the individual is enrolled in self-only coverage or family coverage.

Health FSA Contributions

For plan years beginning on or after Jan. 1, 2013, an employee’s annual pre-tax salary reduction contributions to a health FSA must be limited to $2,500 (as adjusted). The $2,500 limit was increased to:

- $2,550 for 2015 and 2016;

- $2,600 for 2017;

- $2,650 for 2018;

- $2,700 for 2019; and

- $2,750 for 2020.

The IRS has not yet released the FSA dollar limit for taxable years beginning in 2021. The IRS typically announces whether the limit will be adjusted for the next year toward the end of the year.

The limit does not apply to non-elective employer contributions to the health FSA (such as matching contributions or flex credits), though employer contributions that employees may elect to receive in cash or as a taxable benefit will count toward the limit. Other ACA requirements may impact or limit the total amount that may be contributed to a health FSA, but non-elective employer contributions generally do not reduce the health FSA limit for the employee. Additionally, the health FSA limit does not impact contributions under other employer-provided coverage. For example, employee salary reduction contributions to an FSA for dependent care or adoption care assistance are not affected by the health FSA limit.

Update your health FSA’s contribution limit:

- Work with your advisors to monitor IRS guidance on the health FSA limit for 2021.

- Once the 2021 health FSA limit is announced, confirm that your health FSA will not allow employees to make pre-tax contributions in excess of the limit for the 2021 plan year.

- If the 2021 limit is announced too late for your open enrollment, you can use the 2020 limit to ensure compliance.

- Communicate the health FSA limit to employees as part of the open enrollment process.

Summary of Benefits and Coverage (SBC)

Health plans and health insurance issuers must provide an SBC to applicants and enrollees to help them understand their coverage and make coverage decisions. Plans and issuers must provide the SBC to participants and beneficiaries who enroll or re-enroll during an open enrollment period, as well as to participants and beneficiaries who enroll other than through an open enrollment period (including individuals who are newly eligible for coverage and special enrollees).

The SBC must follow strict formatting requirements. The Departments of Health and Human Services, Labor and the Treasury (Departments) provided templates and related materials, including instructions and a uniform glossary of coverage terms, for use by plans and issuers. On Nov. 8, 2019, the Departments issued an updated template and related materials for the SBC. These materials are required to be used for plan years beginning on or after Jan. 1, 2021.

This means that the updated template must be used for the 2021 plan year’s open enrollment period.

Provide the appropriate SBC template:

- For self-funded plans, the plan administrator is responsible for creating and providing the SBC.

- For insured plans, the issuer is required to provide the SBC to the plan sponsor. Both the plan and the issuer are obligated to provide the SBC, although this obligation is satisfied for both parties if either one provides the SBC. If you have an insured plan, confirm whether your health insurance issuer will assume responsibility for providing the SBCs.

Employer Shared Responsibility Rules

Under the ACA’s employer shared responsibility rules, applicable large employers (ALEs) are required to offer affordable, minimum value (MV) health coverage to their full-time employees (and dependent children) or pay a penalty. These employer shared responsibility requirements are also known as the “employer mandate” or “pay or play” rules.

An ALE will be subject to penalties if one or more full-time employees receive a subsidy for purchasing health coverage through an Exchange. An individual may be eligible for an Exchange subsidy either because the ALE does not offer coverage to that individual, or offers coverage that is “unaffordable” or does not provide “minimum value.”

This checklist will help you evaluate your possible liability for a pay or play penalty for 2021. Please keep in mind that this summary is a high-level overview of these rules. It does not provide an in-depth analysis of how the rules will affect your organization. Please contact Reseco Group for more information on these rules and how they may apply to you.

Applicable Large Employer Status

The ACA’s employer shared responsibility rules apply only to ALEs. ALEs are employers with 50 or more full-time employees (including full-time equivalent employees, or FTEs) on business days during the preceding calendar year. Employers determine each year, based on their current number of employees, whether they will be considered an ALE for the following year.

Determine your ALE status for 2021:

- Calculate the number of full-time employees for each calendar month in 2020. A full-time employee is one who is employed, on average, at least 30 hours of service per week or 130 hours for the calendar month.

- Calculate the number of FTEs for each calendar month in 2020 by calculating the aggregate number of hours of service (but not more than 120 hours for any employee) for all employees who were not full-time employees for that month and dividing the total hours of service by 120.

- Add the number of full-time employees and FTEs (including fractions) calculated above for each month in 2020. Add up these monthly numbers and divide the sum by 12. Disregard fractions.

- If your result is 50 or more, you are likely an ALE for 2021.

- Keep in mind that there is a special exception for employers with seasonal workers. If your workforce exceeds 50 full-time employees (including FTEs) for 120 days or fewer during the 2020 calendar year, and the employees in excess of 50 who were employed during that time were seasonal workers, you will not be an ALE for 2021.

- Companies under common ownership may have to be combined to determine their ALE status.

Offering Coverage to Full-time Employees

To correctly offer coverage to full-time employees, ALEs must determine which employees are full-time employees under the employer shared responsibility rule definition. A full-time employee is an employee who was employed, on average, at least 30 hours of service per week (or 130 hours of service in a calendar month).

The IRS provided two methods for determining full-time employee status for purposes of offering coverage—the monthly measurement method and the look-back measurement method.

Monthly Measurement Method

Involves a month-to-month analysis where full-time employees are identified based on their hours of service for each month. This method is not based on averaging hours of service over a prior measurement method. Month-to-month measuring may cause practical difficulties for employers that have employees with varying hours or employment schedules, and could result in employees moving in and out of employer coverage on a monthly basis.

Look-Back Measurement Method

An optional safe harbor method for determining full-time status that can provide greater predictability for determining full-time status. The details of this method are based on whether the employees are ongoing or new, and whether new employees are expected to work full time or are variable, seasonal or part time.

This method involves a measurement period for counting hours of service, an administrative period that allows time for enrollment and disenrollment, and a stability period when coverage may need to be provided, depending on an employee’s average hours of service during the measurement period.

If an employer meets the requirements of the safe harbor, it will not be liable for penalties for employees who work full time durin ey did not work full-time hours during the measurement period.

Determine your full-time employees:

- Use the monthly measurement method or the look-back measurement method to confirm that health coverage will be offered to all full-time employees (and dependent children). If you have employees with varying hours, the look-back measurement method may be the best fit for you.

- To use the look-back measurement method, you will need to select your measurement, administrative and stability periods. Please contact Reseco Group for more information.

Applicable Penalties

An ALE is only liable for a penalty under the employer shared responsibility rules if at least one full-time employee receives a subsidy for coverage purchased through an Exchange. Employees who are offered health coverage that is affordable and provides MV are generally not eligible for these Exchange subsidies.

Depending on the circumstances, one of two penalties may apply under the employer shared responsibility rules—the 4980H(a) penalty or the 4980H(b) penalty.

The 4980H(a) Penalty—Penalty for ALEs not Offering Coverage

Under Section 4980H(a), an ALE will be subject to a penalty if it does not offer coverage to “substantially all” full-time employees (and dependents) and any one of its full-time employees receives a premium tax credit or cost-sharing reduction toward his or her Exchange plan. The 4980H(a) penalty will not apply to an ALE that intends to offer coverage to all of its full-time employees, but that fails to offer coverage to a few of these employees, regardless of whether the failure to offer coverage was inadvertent.

An ALE will satisfy the requirement to offer minimum essential coverage to “substantially all” of its full-time employees and their dependents if it offers coverage to at least 95%—or fails to offer coverage to no more than 5% (or, if greater, five)—of its full-time employees (and dependents). According to the IRS, the alternative margin of five full-time employees is designed to accommodate relatively small ALEs, because a failure to offer coverage to a handful of full-time employees might exceed 5% of the ALE’s full-time employees.

Under the ACA, the monthly penalty assessed on ALEs that do not offer coverage to substantially all full-time employees and their dependents is equal to the ALE’s number of full-time employees (minus 30) X 1/12 of $2,000 (as adjusted), for any applicable month. After 2014, the $2,000 amount is indexed for the calendar year, as follows:

The 4980H(b) Penalty—Penalty for ALEs Offering Coverage

ALEs that do offer coverage to substantially all full-time employees (and dependents) may still be subject to penalties if at least one full-time employee obtains a subsidy through an Exchange because:

• The ALE did not offer coverage to all full-time employees; or

• The ALE’s coverage is unaffordable or does not provide minimum value.

The monthly penalty assessed on an ALE for each full-time employee who receives a subsidy is 1/12 of $3,000 (as adjusted) for any applicable month. However, the total penalty for an ALE is limited to the 4980H(a) penalty amount. After 2014, the $3,000 amount is indexed as follows:

Affordability of Coverage

Under the ACA, an ALE’s health coverage is considered affordable if the employee’s required contribution to the plan does not exceed 9.5% of the employee’s household income for the taxable year (as adjusted each year). The adjusted percentage is 9.83% for 2021. “Household income” means the modified adjusted gross income of the employee and any members of the employee’s family. Because an employer generally will not know an employee’s household income, the IRS provided three affordability safe harbors that ALEs may use to determine affordability based on information that is available to them. These safe harbors allow an ALE to measure affordability based on the employee’s Form W-2 wages, the employee’s rate of pay or the federal poverty level for a single individual. ALEs using an affordability safe harbor may rely on the adjusted affordability contribution percentages.

Minimum Value

Under the ACA, a plan provides MV if the plan’s share of total allowed costs of benefits provided under the plan is at least 60% of those costs. Three approaches may be used for determining MV: a Minimum Value (MV) Calculator, design-based safe harbor checklists or actuarial certification. In addition, any plan in the small group market that meets any of the “metal levels” of coverage (that is, bronze, silver, gold or platinum) provides MV.

In addition, plans that do not provide inpatient hospitalization or physician services (referred to as non-hospital/non- physician services plans) do not provide MV. An employer may not use the MV Calculator (or any actuarial certification or valuation) to demonstrate that a non-hospital/non-physician services plan provides MV. As a result, a non-hospital/non-physician services plan should not be adopted for the 2015 plan year or beyond.

Calculate potential penalties for 2020 and/or 2021:

Review the cost of your health plan coverage to determine whether it’s affordable for your employees by using one or more of the affordability safe harbors.

- Determine whether the plan provides MV by using one of the four available methods.

- Calculate any penalties that may apply under these rules using the formulas above.

Reporting of Coverage

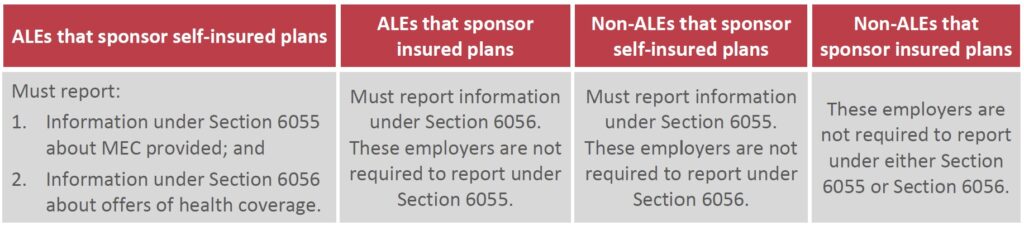

The ACA requires ALEs to report information to the IRS and to their full-time employees regarding the employer-sponsored health coverage they offer. The IRS will use the information that ALEs report to verify employer-sponsored coverage and administer the employer shared responsibility provisions. This reporting requirement is found in Code Section 6056.

The ACA also requires every health insurance issuer, sponsor of a self-insured health plan, government agency that administers government-sponsored health insurance programs and any other entity that provides MEC to file an annual return with the IRS reporting information for each individual who is provided with this coverage. Related statements must also be provided to individuals. This reporting requirement is found in Code Section 6055.

The IRS has provided relief from the penalty for failing to furnish a statement to individuals as required under Section 6055 for 2019 and 2020 in certain cases. Specifically, the penalty for failing to furnish a Form 1095-B to responsible individuals will not apply in cases where the reporting entity:

- Prominently posts a notice on its website stating that responsible individuals may receive a copy of their 2019 or 2020 Form 1095-B, as applicable, upon request; and

- Furnishes a 2019 or 2020 Form 1095-B, as applicable, to any responsible individual upon request within 30 days of the date the request is received.

The individual mandate penalty has been reduced to zero, beginning in 2019. As a result, an individual does not need the information on Form 1095-B in order to calculate his or her federal tax liability or file a federal income tax return. However, reporting entities required to furnish Form 1095-B to individuals must continue to expend resources to do so.

Both of these reporting requirements took effect in 2015. Returns are due in early 2021 for health plan coverage offered or provided in 2020.

- Returns generally must be filed with the IRS by Feb. 28 (or March 31, if filed electronically) of the year after the calendar year to which the returns relate. For the 2020 calendar year, returns must be filed by March 1, 2021 (since Feb. 28 is a Sunday), or March 31, 2021, if filed electronically.

- Written statements generally must be provided to employees no later than Jan. 31 of the year following the calendar year in which coverage was provided. For the 2020 calendar year, the deadline to furnish individual statements was set to be Feb. 1, 2021 (since Jan. 31 is a Sunday). However, the IRS has provided an additional 30 days for furnishing the 2020 Form 1095-B and Form 1095-C, extending the due date to March 2, 2021.

ALEs with self-funded plans are required to comply with both reporting obligations, while ALEs with insured plans will only need to comply with Section 6056. To simplify the reporting process, the IRS allows ALEs with self-insured plans to use a single combined form for reporting the information required under both Section 6055 and 6056.

Forms Used for Reporting

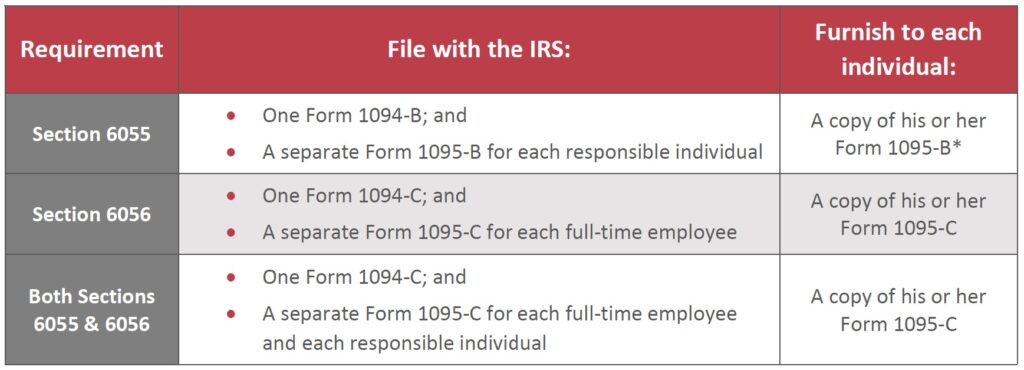

Under both Sections 6055 and 6056, each reporting entity must file all of the following with the IRS:

- A separate statement for each individual; and

- A single transmittal form for all of the returns filed for a given calendar year.

Under Section 6055, reporting entities will generally file Forms 1094-B (a transmittal) and 1095-B (an information return). Under Section 6056, entities will file Forms 1094-C (a transmittal) and 1095-C (an information return) for each full-time employee for any month. Entities that are reporting under both Sections 6055 and 6056 will file using a combined reporting method, on Form 1094-C and Form 1095-C.

*Note, though, that penalty relief is available for 2019 and 2020 calendar year reporting under certain circumstances for reporting entities that furnish Forms 1095-B to responsible individuals only upon request.

Electronic Reporting

Any reporting entity that is required to file at least 250 returns under Section 6055 or Section 6056 must file electronically. The 250-or-more requirement applies separately to each type of return and separately to each type of corrected return. Entities filing fewer than 250 returns during the calendar year may choose to file in paper form, but are permitted (and encouraged) to file electronically. Electronic filing will be done using the ACA Information Returns (AIR) Program. More information on the AIR Program is available on the IRS website.

Individual statements may also be furnished electronically if certain notice, consent and hardware and software requirements are met (similar to the process currently in place for the electronic furnishing of employees’ Forms W-2).

Penalties

A reporting entity that fails to comply with the Section 6055 or Section 6056 reporting requirements may be subject to the general reporting penalties for failure to file correct information returns (under Code Section 6721) and failure to furnish correct payee statements (under Code Section 6722).

Penalties may be waived if the failure is due to reasonable cause and not to willful neglect, or may be reduced if the failure is corrected within a certain period of time. Also, lower annual maximums apply for reporting entities that have average annual gross receipts of up to $5 million for the three most recent taxable years. The penalty amounts for failures related to returns and statements required to be filed or furnished in 2021 have not been released at this time. The penalty amounts for returns and statements required to be filed or furnished in 2020 are as follows:

*For failures due to intentional disregard, the penalty is equal to the greater of either the listed penalty amount or 10% of the aggregate amount of the items required to be reported correctly.

Prepare for health plan reporting:

- Determine which reporting requirements apply to you and your health plans.

- Determine the information you will need for reporting and coordinate internal and external resources to help compile the required data.

- Complete the appropriate forms. Furnish statements to individuals on or before Feb. 1, 2021, and file returns or before March 1, 2021 (March 31, 2021, if filing electronically).

Employee Notice of Exchange

Employers are required to provide all new hires with a written notice about the ACA’s health insurance Exchanges. This notice must be provided at the time of hiring. In general, the notice must:

- Inform employees about the existence of the Exchange and describe the services provided;

- Explain how employees may be eligible for a premium tax credit or a cost-sharing reduction if the employer’s plan does not meet certain requirements; and

- Inform employees that if they purchase coverage through the Exchange, they may lose any employer contribution toward the cost of employer-provided coverage, and that all or a portion of the employer contribution to employer-provided coverage may be excludable for federal income tax purposes.

The DOL provided model Exchange notices for employers to use, which will require some customization. The notice may be provided by first-class mail, or may be provided electronically if the requirements of the DOL’s electronic disclosure safe harbor are met.

Ensure that the Exchange notice is provided to all new hires at the time of hiring:

- Customize the appropriate model Exchange notice.

- Confirm that the notice has been provided to all current employees.

- Prepare to provide the customized notice to all new employees when hired.

This Compliance Overview is not intended to be exhaustive nor should any discussion or opinions be construed as legal advice. Readers should contact legal counsel for legal advice. ©2020 Zywave, Inc. All rights reserved.

More like this:

Final Forms And Instructions For 2020 ACA Reporting Released